An Industrial boom is underway in America

According to a recent article from the Financial Times (April 2023), more than $200bn in large scale manufacturing projects have been committed by companies since Congress passed the Chips Act and the Inflation Reduction Act last year. This could be the beginning of a new industrial boom in America. That's great news for the country.

The Financial Times trackedmore than 75 manufacturing projects worth at least $100mn eachthat have been announced since the bills became law in August. These large scale projects are for plants to make semiconductors, electric vehicles, batteries, and renewable energy components. These announcements will create around 82,000 jobs.

This manufacturing boom bodes well for a company like the one featured in this article. It's a company with a pristine balance sheet and strong free cash flows. An American company that has been around since 1917 and has a proven track record of excellent returns.

GLOBAL MANUFACTURER

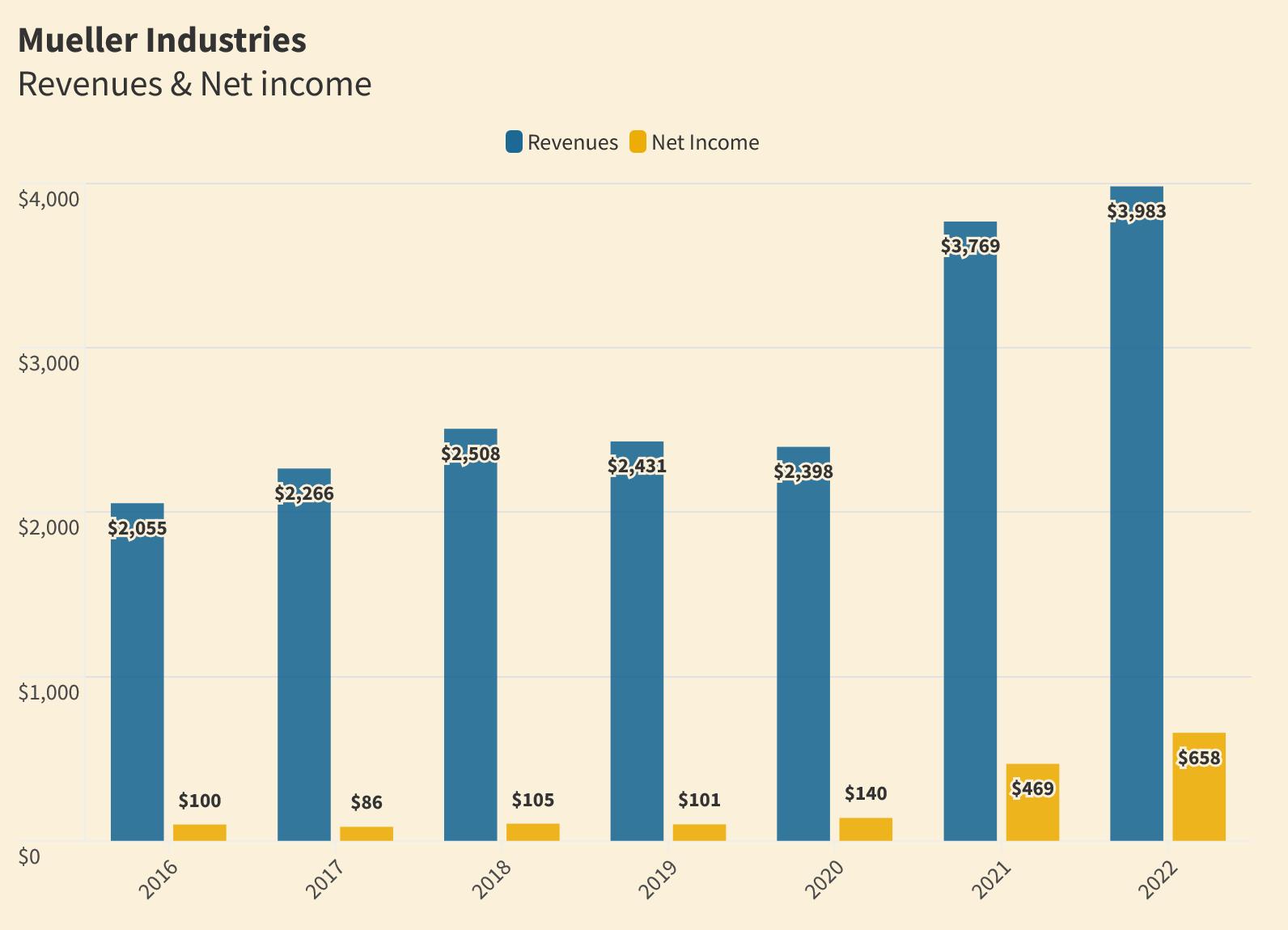

Mueller Industries (NYSE:MLI, $76.76) is an industrial manufacturer that specializes in copper and copper alloy manufacturing. It also produces goods made from aluminum, steel and plastics. The company is headquartered in Collierville, Tennessee. The company has operations in North America, Europe, Asia and the Middle East. Its products include tubing, fittings, valves and similar items for plumbing and HVACR related piping systems, as well as rod, forgins, extrusions, and various components for OEM applications.

In the most recent quarter, the company reported $971 million in net sales and $173 million in profits. Cash flows from operations for the quarter were $112 million. Capital expenditures for the quarter were $7.5 million. Free cash flows for the period were $104 million. The balance sheet is impressive. $782 million in cash and short-term investments at the end of the quarter. Long-term debt is pretty much nil at $2.4 million. Shares outstanding are 56.4 million.

The company's products are distributed into sectors such as building construction, appliance, defence, energy, and automotive. These products can be found as critical components in applications ranging from potable water distribution to automotive drive trains to household appliances to radar defense systems, and more. Sales are categorized into the following business segments: Piping Systems, Climate Products and Industrial Metals.

Sales by segment

Gross Margins

% of Sales by geography

Click on graph for % per region