At current oil prices, this oil producer is gushing cash flows.

While oil is often regarded as a "dirty" resource, its significance and relevance persist in the foreseeable future. Despite the ongoing initiatives by developed nations to shift towards green energy, oil maintains its status as the predominant global energy source. It continues to power transportation systems, industries, and economies worldwide. With its abundant supply and high energy density, oil serves as an efficient and easily accessible fuel for critical sectors such as aviation, shipping, manufacturing, and notably, the military. Additionally, oil plays a vital role in electricity generation, particularly in regions heavily reliant on fossil fuels.

Oil also serves as a fundamental raw material for countless industries. The petrochemical sector heavily relies on oil as a feedstock for producing plastics, synthetic fibers, fertilizers, and pharmaceuticals. These products are integral components of modern society, with applications in construction, packaging, textiles, agriculture, and healthcare. As such, the continued relevance of oil extends beyond its role as an energy source, making it an essential driver of economic growth, innovation, and technological advancement.

In this article, we will look at a prominent oil producer located in South America. This particular company has been on my radar for almost a year, and I have been eagerly awaiting a decline in its share price to seize a more favorable entry point. So far though, the stock has experienced nothing but a consistent upward trajectory since I started following it. I remain confident that exercising patience will eventually pay off and lead to a pullback, enabling me to acquire it at a more advantageous price.

Parex is an independent exploration and production company in Colombia, focusing on sustainable, conventional oil and gas production.

Parex Resources, a prominent independent oil and gas exploration and production company, has established itself as a key player in Colombia's energy landscape. It is now the largest independent oil producer in the country. With a focus on operational excellence and a robust portfolio of assets, Parex Resources continues to deliver impressive financial performance.

In addition to its operational achievements, Parex Resources has demonstrated a solid financial foundation. The company's revenues have witnessed steady growth, propelled by increased production levels and favorable oil prices. With a disciplined approach to capital allocation and debt management, Parex Resources maintains a strong balance sheet, further enhancing its financial stability. As the company continues to prioritize sustainability and social responsibility, Parex Resources is poised to deliver long-term value to its shareholders while contributing to the development of local communities.

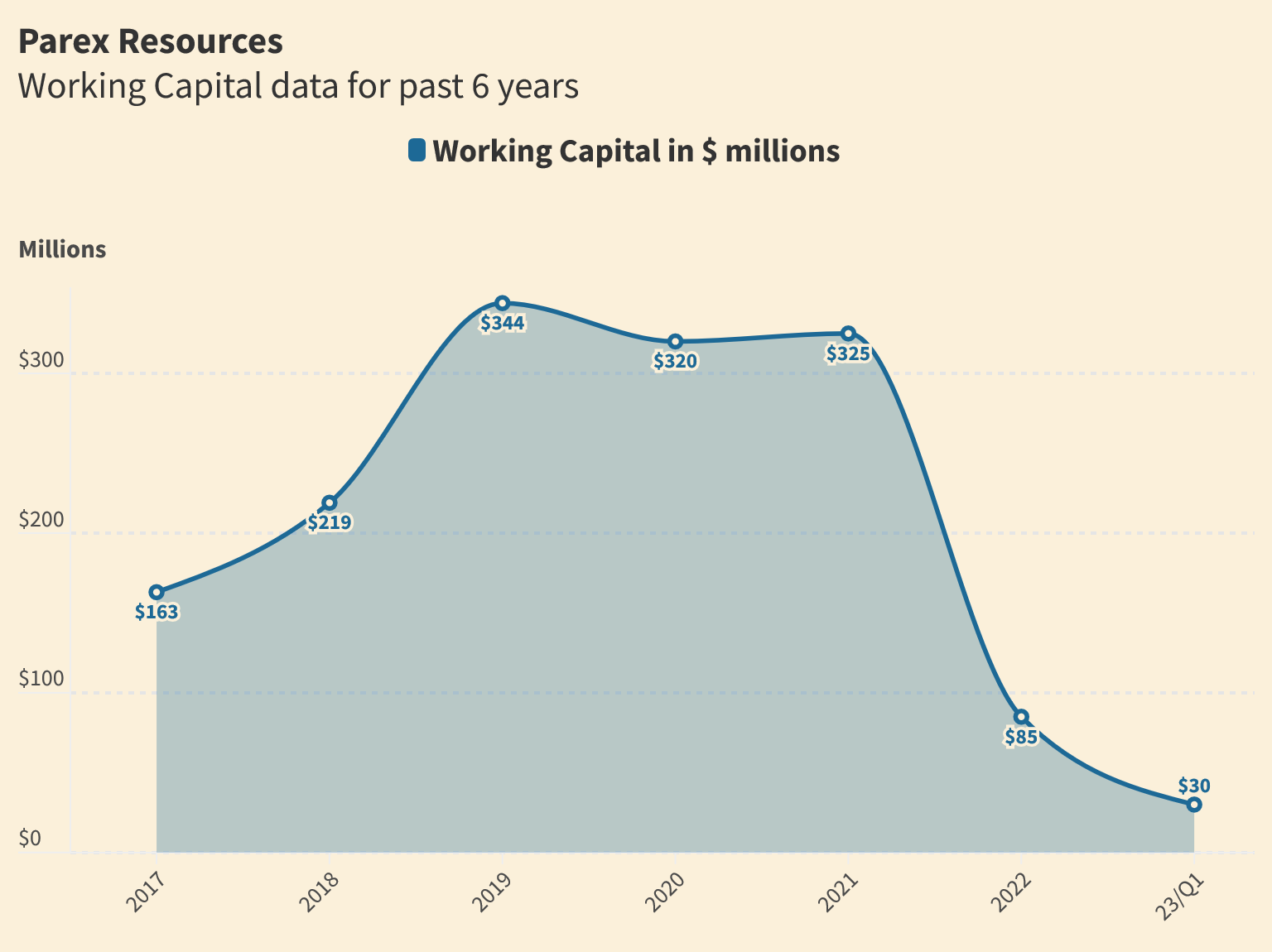

For the most recent quarter, Parex Resources delivered a robust financial performance. The company reported record-high revenues and strong cash flow generation, indicating its ability to capitalize on increased production levels and favorable oil prices. Parex Resources maintained a low-cost structure, allowing it to weather market fluctuations and deliver consistent profitability. The company's disciplined approach to capital allocation and debt management contributed to a solid balance sheet. The company boasts a debt-free balance sheet, a large cash pile of USD $372 million and positive free cash flows. Overall, Parex Resources' financial performance in the most recent quarter reflects its strong position in the energy sector and its commitment to creating long-term value for shareholders.

Q1 Highlights

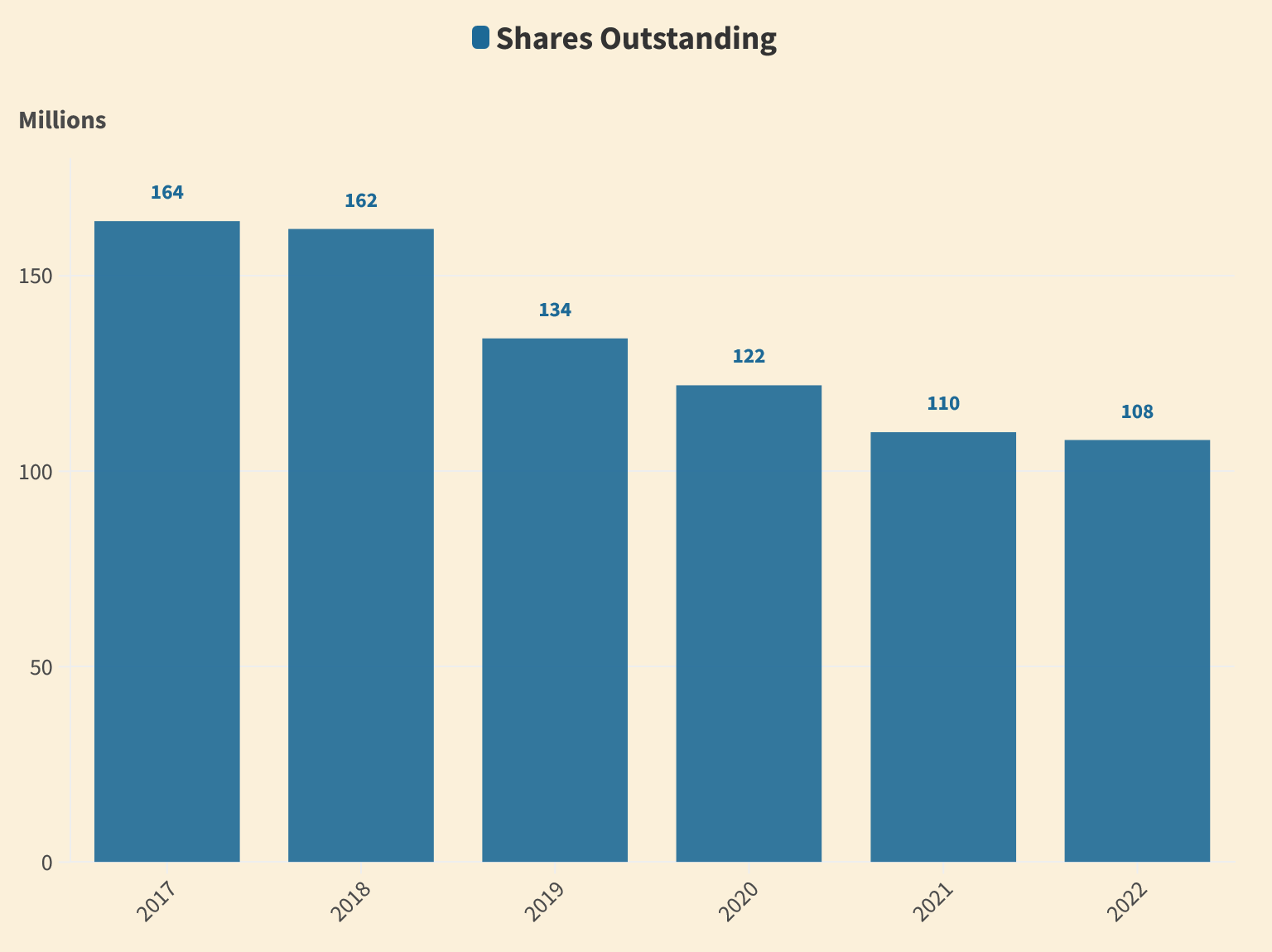

The company has achieved remarkable success in reducing its outstanding shares. In 2017, the number of shares stood at approximately 165 million, which has significantly decreased to 107 million as of the end of Q1/2023, representing a 35% decrease over six years. Additionally, the company initiated a quarterly dividend two years ago, currently amounting to $0.37 per share per quarter. This equates to an annual dividend of $1.50 per share, resulting in a respectable yield of 5.25%. The management has expressed their intention to distribute 100% of the 2023 free funds flow to shareholders through dividends and buybacks.

Despite the decline in oil prices since their peak in March 2022, the company's stock has experienced a remarkable surge over the past six months. It has surged from $17.94 in December 2022 to $28.51 at the closing on June 2nd, 2023, marking a 50% increase in a short period of time. Even at these elevated prices, the stock maintains a low P/E (Price-to-earnings) multiple of less than 6 times, which indicates favorable valuation.